June 27, 2026adminUncategorizedComments Off on How Management Consulting Firms Can Get Paid Faster with ACH & Card Processing

Cash flow is one of the most important factors in running a successful consulting business.

Delayed payments mean delayed growth.

Whether you’re a management consultant, financial advisor, or accounting firm, offering modern payment options can significantly improve your collections.

PayGen offers payment solutions built for professional service businesses, including:

ACH & eCheck processing

Credit card acceptance

Merchant accounts

Virtual terminal

Payment gateway solutions

Recurring billing tools

Whether your clients prefer paying by bank account or credit card, PayGen gives your business the flexibility to accept payments securely and efficiently.

Looking for a payment solution that fits your consulting business? Contact PayGen today and start accepting ACH, eCheck, and card payments with confidence.

Many consulting firms automatically accept credit cards because that’s what clients expect. However, as invoice values increase, card payments become more expensive.

For years, financial consulting firms have relied on paper checks, wire transfers, and credit cards to collect payments. While these methods still work, they often come with unnecessary costs, delays, and administrative overhead.

Today, more firms are adopting ACH and eCheck payments as a faster, more cost-effective way to collect large invoices.

Unlike credit card payments, ACH transactions move funds directly between bank accounts. This makes them ideal for businesses that regularly invoice clients for thousands of dollars.

Benefits include:

Lower processing costs

Simple payment collection

Better cash flow management

Secure bank-to-bank transfers

Convenient payment links

Recurring billing for retainers

Perfect for Professional Services

ACH payments are an excellent fit for:

Financial Strategy Firms

Business Consultants

General Management Consultants

Accounting Firms

Tax Advisors

Fractional CFO Services

Legal Firms

If your firm sends invoices ranging from $2,000 to $50,000 or more, ACH payments can simplify collections while reducing payment friction.

May 31, 2026adminUncategorizedComments Off on High Risk Merchant Accounts in the USA: Why Businesses Are Switching to Pay-by-Bank (ACH Payments)

Many US businesses struggle to stay fully operational with traditional payment processors like Stripe, PayPal, or standard acquiring banks.

If your business operates in a high-risk industry, you’ve likely faced:

Sudden account freezes or shutdowns

High chargeback ratios

Payment declines from US banks

Rolling reserves holding your cash flow

Difficulty scaling payments internationally

This is especially common in industries like forex, crypto, CBD, adult services, SaaS subscriptions, and high-ticket coaching.

Because of these challenges, more US merchants are now adopting a more stable alternative: 👉 Pay-by-Bank (ACH payments)apply

What Is a High Risk Merchant Account in the USA?

A high-risk merchant account in the United States is a payment processing setup designed for businesses that traditional banks consider risky due to:

High chargeback potential

Regulatory sensitivity

Large transaction volumes

Cross-border or subscription-based billing

Common US High-Risk Industries:

Forex trading platforms (US-facing or offshore onboarding US clients)

Cryptocurrency exchanges and brokers

CBD and hemp product businesses

Adult content platforms and subscription sites

Credit repair companies

Debt relief services

High-ticket coaching & online education programs

Subscription SaaS with recurring billing

These businesses often experience restricted access to mainstream card processors.

Why Credit Card Processing Fails for High-Risk US Businesses

Even in the United States, card processing is not built for high-risk models.

1. High Chargeback Exposure

US consumers can dispute card transactions easily, creating financial risk for processors.

2. Processor Shutdown Risk

Stripe, PayPal, and similar providers frequently terminate accounts in restricted industries.

3. Rolling Reserves

Many high-risk merchants are forced to keep 5%–20% of revenue frozen for months.

4. Low Approval Rates

Banks often decline transactions linked to:

Crypto activity

Forex deposits

Subscription spikes

International card usage

What Is Pay-by-Bank (ACH Payments)?

Pay-by-Bank in the USA refers to ACH (Automated Clearing House) payments, where funds move directly between bank accounts without using credit or debit cards.

Instead of relying on Visa or Mastercard networks, ACH payments go through the US banking system.

Types of US Bank Payments:

ACH Debit (customer pays you directly)

ACH Credit (you push payments)

Same-day ACH transfers

Bank-to-bank transfers via open banking providers

Why US High-Risk Businesses Are Switching to ACH

1. Higher Payment Approval Rates

ACH transactions are less likely to be declined compared to credit cards.

2. Lower Chargeback Risk

ACH payments are significantly harder to reverse than card payments, reducing fraud exposure.

3. Lower Processing Fees

US businesses save significantly compared to 2.9%–5% card processing fees.

4. Better for Large Transactions

Ideal for:

Forex deposits ($1,000 – $50,000+)

SaaS enterprise billing

Investment platforms

B2B payments

5. More Stable Banking Relationships

ACH reduces dependency on card processors that frequently shut down high-risk accounts.

Industries in the USA That Benefit Most from Pay-by-Bank

Forex & Trading Platforms

Reliable funding for US-based or US-targeted traders.

Crypto Exchanges & Brokers

Reduces dependency on restricted card processors.

CBD & Hemp Businesses

Avoids constant merchant account closures.

SaaS Companies

Reduces failed recurring payments from expired cards.

Subscription & Membership Platforms

Improves payment retention rates.

Credit Repair & Debt Services

Provides stable recurring billing infrastructure.

Pay-by-Bank vs Credit Card Processing in the US

Feature

Credit Cards

Pay-by-Bank (ACH)

Approval rate

Medium / Low

High

Chargebacks

High

Low

Processing fees

2.9%–5%

Much lower

Account shutdown risk

High

Low

Best for large payments

No

Yes

Stability

Unstable

Stable

Why the US Market Is Moving Toward ACH Payments

The shift is happening because:

US banks are tightening high-risk card approvals

Stripe/PayPal enforcement is increasing

Subscription businesses need better retention tools

Cross-border US businesses face higher decline rates

Businesses want lower transaction costs

👉 Result: ACH is becoming the default fallback for high-risk US merchants

How Paygen Supports US High-Risk Merchants

Paygen helps US businesses that struggle with traditional payment processors by providing:

High-risk merchant account solutions

ACH / pay-by-bank payment infrastructure

Alternative processing routes when cards fail

Reduced chargeback exposure systems

Scalable payment setups for US-based operations

We work with industries that traditional processors often reject.

Final Thoughts

For US high-risk businesses, relying solely on credit card processors is no longer sustainable.

The market is clearly shifting toward:

Bank-based payments (ACH) + hybrid payment systems

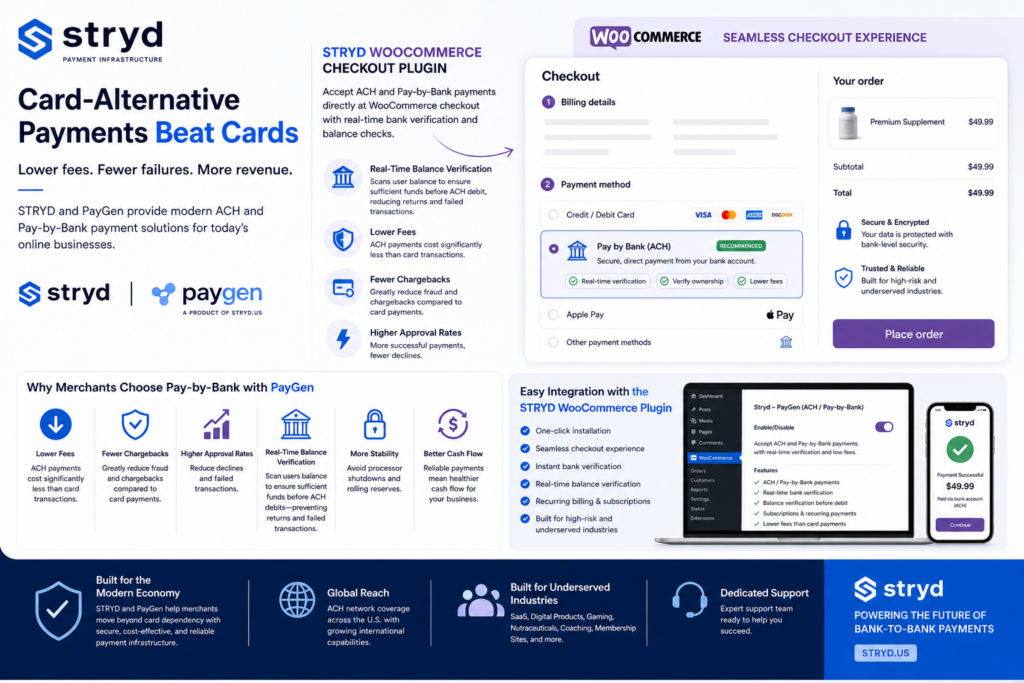

For years, credit and debit cards dominated online payments. They were fast, convenient, and widely accepted. But today, a major shift is happening across eCommerce, SaaS, gaming, subscription businesses, and high-risk industries: merchants are increasingly moving toward card-alternative payments, especially Pay by Bank and ACH-based systems.

The reason is simple — cards are becoming expensive, unstable, and risky for many businesses.

Meanwhile, bank-to-bank payment systems are proving to be faster, more secure, and far more reliable for modern merchants.

Platforms like STRYD and its merchant-facing payment solution PayGen are helping businesses transition away from over-dependence on card networks by offering modern ACH and Pay-by-Bank infrastructure built for today’s internet economy.

The Problem With Traditional Card Payments

Card processing comes with several hidden challenges that most merchants eventually experience:

High transaction fees

Chargebacks and fraud

Sudden account freezes

Rolling reserves

Declined transactions

Processor instability for high-risk industries

For businesses operating in industries like SaaS, nutraceuticals, coaching, peptides, gaming, travel, or digital products, traditional card processors often create more problems than solutions.

Many merchants discover that even legitimate businesses can suddenly lose payment access because banks and card networks classify them as “high risk.”

At the same time, card fraud continues to rise globally, forcing processors to tighten risk controls and increase reserve requirements.

Why Pay-by-Bank Is Growing Fast

Pay-by-Bank allows customers to pay directly from their bank accounts instead of using a card.

Rather than routing payments through Visa or Mastercard rails, the transaction moves through ACH banking infrastructure.

This creates several major advantages:

Lower Processing Costs

ACH and bank payments typically cost merchants significantly less than card transactions. Many businesses save thousands of dollars monthly by reducing card dependency.

Reduced Chargebacks

Unlike cards, ACH transactions generally experience fewer chargeback disputes, which reduces fraud exposure and operational losses.

Better Approval Rates

Card payments fail for many reasons:

Expired cards

Insufficient limits

Fraud filters

International restrictions

Bank payments eliminate many of these issues because they connect directly to verified bank accounts.

Real-Time Bank Verification

Modern Pay-by-Bank systems now use open banking and real-time account verification technologies to verify ownership and confirm available balances before processing payments.

This is where platforms like STRYD stand out.

According to the company’s published infrastructure overview, STRYD uses Plaid-powered bank verification and real-time balance checks to help merchants reduce failed ACH debits and payment returns.

How STRYD and PayGen Are Changing Payment Processing

PayGen is a merchant payment solution built on top of STRYD’s ACH and Pay-by-Bank infrastructure.

Instead of relying only on traditional card rails, Stryd gives merchants access to:

ACH / Pay-by-Bank payments

Real-time balance verification

Bank account authentication

Fraud screening

AI-powered risk analysis

WooCommerce integration

API-based payment infrastructure

Support for underserved industries

The system is especially useful for merchants that struggle with processor shutdowns or high chargeback environments.

STRYD states that its infrastructure was specifically designed to support industries often rejected by mainstream processors, including nutraceuticals, SaaS, gaming, digital products, and subscription businesses.

Consumers Are Already Comfortable With Bank Payments

Many users already interact with ACH-powered systems daily without realizing it.

Payroll deposits, subscription billing, bank transfers, peer-to-peer apps, and many fintech platforms rely heavily on ACH infrastructure. Community discussions across fintech and banking forums frequently point out that services like Venmo, bank transfer apps, and business payment systems already use ACH rails behind the scenes.

This means consumers are increasingly comfortable linking bank accounts directly for payments — especially when the checkout experience is instant and secure.

The Future of Payments Is Bank-to-Bank

Cards are not disappearing anytime soon. But the market is clearly evolving toward hybrid payment ecosystems where merchants offer both cards and direct bank payments.

The businesses adapting early are gaining advantages through:

Lower fees

Higher approval rates

Better stability

Reduced fraud exposure

Improved cash flow

As open banking adoption grows globally, Pay-by-Bank is expected to become one of the most important payment methods in eCommerce and digital business.

Platforms like STRYD and PayGen are positioning themselves at the center of that transition by helping merchants move beyond traditional card dependency and into the next generation of payment infrastructure.

WooCommerce Checkout

STRYD also offers a dedicated WooCommerce checkout plugin that allows merchants to integrate ACH and Pay-by-Bank payments directly into their store checkout flow without requiring complex custom development.

The plugin enables merchants to:

Accept ACH and Pay-by-Bank payments directly at checkout

Verify customer bank accounts instantly

Perform real-time balance verification before ACH debits

Reduce failed payments and insufficient-fund returns

Offer alternative payment methods alongside cards

Create smoother subscription and recurring billing experiences

For WooCommerce merchants, this means customers can complete payments directly from their bank accounts through a modern checkout experience while merchants benefit from lower fees, fewer chargebacks, and more stable payment processing.

The integration is especially valuable for:

SaaS businesses

Subscription platforms

Digital services

Online coaching businesses

eCommerce stores

High-risk merchants seeking alternatives to traditional card processors

Instead of relying entirely on Visa or Mastercard rails, merchants can now add a bank-to-bank payment option directly inside their WooCommerce checkout using STRYD’s infrastructure powered through .

In the coming years, the question may no longer be: “Do you accept cards?”

Instead, it may become: “Why are you still relying on them alone?”

Stryd by PayGen is redefining how businesses accept payments with secure, real-time pay-by-bank infrastructure. Built for high-risk industries, Stryd leverages powerful integrations like Plaid to enable instant bank payments, reduce fraud, eliminate chargebacks, and lower processing costs—giving businesses a smarter, more reliable way to scale globally.

Struggling to process payments in a high-risk industry? PayGen delivers reliable, scalable payment solutions tailored for businesses that traditional processors reject. From credit cards and ACH to advanced pay-by-bank solutions powered by Plaid and Stryd, we help you reduce chargebacks, lower fees, and accept payments globally with confidence.

If you’ve received that dreaded message — “Your account has been permanently limited” or “We’ve deactivated your Stripe account” — you’re not alone.

Thousands of business owners and entrepreneurs find themselves banned from PayPal or Stripe each year, often without warning. Whether you’re running a dropshipping store, a high-risk business, or selling digital products, losing your payment processor can feel like hitting a wall.

But here’s the good news: you don’t have to shut down your business. At Paygen, we specialize in helping banned or high-risk merchants get back to accepting payments fast — without the red tape.

⚠️ Why Stripe and PayPal Ban Accounts

Both platforms are known for strict risk and compliance policies. Here are common reasons businesses get banned:

Selling “high-risk” products like CBD, supplements, adult content, forex, or coaching services

Using PayPal for dropshipping or non-traditional fulfillment methods

Chargeback rates that exceed platform limits

Recurring/subscription models flagged by Stripe

Sudden spikes in sales volume

Operating from a country not supported by PayPal or Stripe

If any of this sounds familiar, you’re likely searching for:

PayPal banned me, Stripe account deactivated, high-risk merchant account, alternative to PayPal, Stripe replacement, payment processor for banned users

✅ What to Do After Getting Banned

Instead of scrambling for workarounds or setting up another account that might get banned again, you need a real, stable solution.

That’s where Paygen comes in.

We help merchants who’ve been:

Banned from PayPal or Stripe

Flagged for high-risk activity

Operating in restricted regions

Running subscription or recurring businesses

With us, you can access:

A fully functional merchant account

eCheck/ACH solutions for U.S. clients

Credit card processing for CBD, adult, coaching, finance, crypto, and more

Support for merchants from the US, UK, Canada, Nigeria, UAE, and other regions

🔁 Accept Payments Again — In 24 to 72 Hours

Paygen offers a seamless onboarding process. You don’t need to “hide” your business model or lie about your industry — we work with honest, transparent risk categories.

We believe every business deserves a way to get paid, no matter the niche. That’s why Paygen is trusted by coaches, adult businesses, digital service providers, and ecommerce entrepreneurs who’ve been left behind by traditional processors.

🔗 Ready to Get Started?

Don’t let PayPal or Stripe determine your business future. Join hundreds of merchants who made the switch to Paygen.

June 24, 2025adminUncategorizedComments Off on Paygen ACH & eCheck Payment Processing – High-Ticket, Unlimited Volume Bank Debits Made Easy

As digital payments evolve, many businesses are discovering that card processors don’t always meet their needs — especially when it comes to large transactions, predictable costs, or operating in high-risk industries. That’s where Paygen comes in.

We offer a powerful ACH and eCheck payment processing solution designed to give your business more control, fewer limits, and better margins — with unlimited monthly volume and ticket sizes up to $10,000 per transaction.

👉 Click here to apply or contact us for a custom ACH or eCheck solution built around your business.

💡 Why Choose Paygen for ACH & eCheck Payment Processing?

✅ Unlimited Monthly Processing Volume No matter how fast your business is growing, we won’t cap your potential. Our ACH debit and eCheck payment systems are designed to scale with you — whether you’re processing a few high-value transactions or thousands of smaller ones.

✅ High-Ticket Transactions – Up to $10,000 Each Processing big invoices? High-value sales? With Paygen, you can accept single ACH payments or eChecks up to $10,000, eliminating the need to split transactions or deal with excessive card fees.

✅ Low-Cost Bank Debit Solution Avoid high interchange fees. ACH and bank debit transactions typically cost far less than credit card processing. That means more revenue stays in your business.

✅ Ideal for High-Risk and High-Growth Businesses From CBD and nutraceuticals to digital services and coaching, we support industries that traditional processors shy away from. Paygen makes ACH debit and credit transactions easy, even for businesses considered high-risk.

✅ Full Support for ACH Credit & Debit Whether you’re pulling funds from customers (ACH debit) or sending payouts to partners or vendors (ACH credit), we provide a seamless way to manage it all in one platform.

✅ eCheck Payment Compatibility Don’t want to require login to online banking? No problem. Our eCheck payment solution lets your customers pay using just their routing and account number — making the checkout process fast and intuitive.

🔁 ACH Payment vs. eCheck: What’s the Difference?

Both ACH and eCheck payments move funds electronically between banks. The main difference is the method of initiation. ACH payments are usually processed in batches and scheduled ahead, while eChecks are digital versions of paper checks, offering a familiar experience with faster clearing times.

With Paygen, you can accept both — giving your clients flexibility and giving you more ways to get paid.

🚀 Fast, Flexible, and Secure

Quick onboarding – Get approved and start processing in days

NACHA-compliant – Stay on top of industry security standards

API & hosted checkout options – Easy integration for any business model

Same-day ACH available (optional) – For even faster settlement

If you’re ready to accept ACH payments, bank debits, or eCheck payments with no volume caps, high ticket size limits, and simple pricing — Paygen is the right partner.

👉 Click here to apply or contact us for a custom ACH or eCheck solution built around your business.

Paygen – Smart Payment Processing and Gateway Services Your trusted partner for ACH credit, ACH debit, and eCheck payment processing with unlimited volume and high-value support.

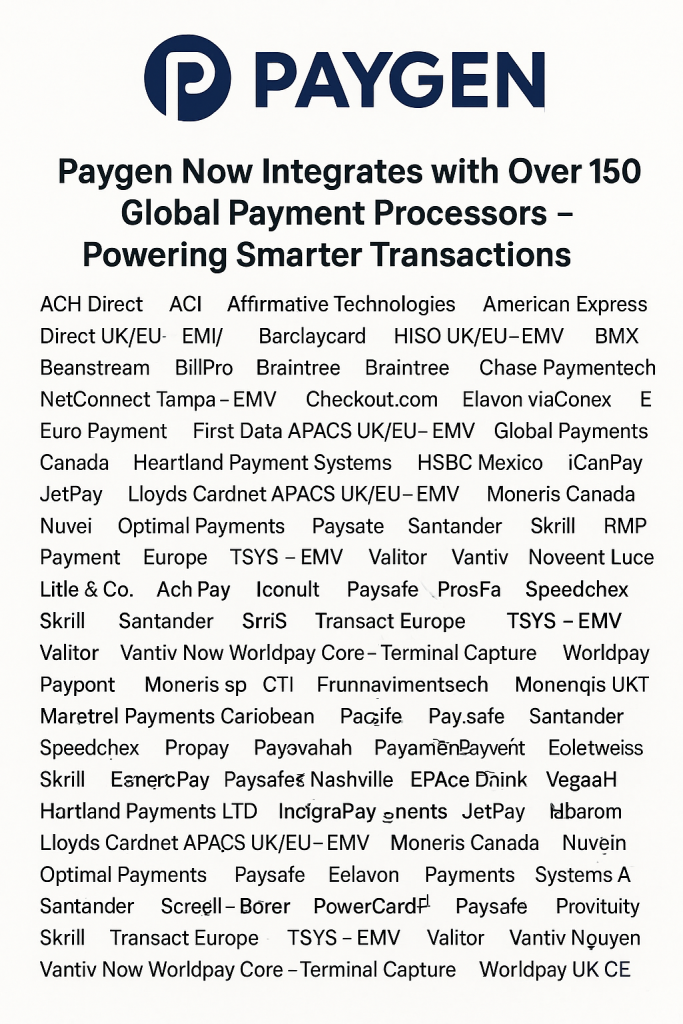

May 2, 2025adminUncategorizedComments Off on Paygen Now Integrates with Over 150 Global Payment Processors – Powering Smarter Transactions

In today’s dynamic digital economy, businesses need agile and scalable payment solutions that don’t lock them into limited processing options. That’s why we’re proud to announce that Paygen now supports integration with over 150 payment processors worldwide, giving merchants unprecedented flexibility, control, and freedom in how they accept payments.

🧠 What This Means for You

Whether you’re a high-risk merchant, a subscription-based service, or a fast-scaling eCommerce brand, you can now:

Choose the processor that fits your risk profile and regional needs

Work with multiple processors simultaneously to increase redundancy

Connect seamlessly via Paygen’s unified payment gateway interface

Scale globally without worrying about processor limitations

🔌 Extensive Processor Compatibility

From industry giants like Chase Paymentech, First Data, WorldPay, BlueSnap, and Skrill, to niche and regional options like BrasPag, Chronopay, and PACNET, we’ve ensured that Paygen is compatible with a wide array of platforms. Below is our full list of supported processors:

AccessOffshore.net, ACH Direct, ACI, AffiPay, Affirmative Technologies, AIBMS APACS UK/EU – EMV, Allied System v2, Alternative Payments International, American Express Direct UK/EU – EMV, Barclaycard HISO UK/EU – EMV, Beanstream, BillPro, BlueSnap, BlueSnap Dev, BluSky, Borgun, Braintree, BrasPag, BrasPag V2, BroadPay, Caledon, Cardley, CardWorks, Cashflows, Chain Commerce, Chase Paymentech NetConnect Tampa – EMV, Chase Paymentech Salem, Chase Paymentech Salem – EMV, Chase Paymentech Tampa, Check By Phone, CheckGateway, Checkout.com, Checkout.com 3.0, Checkout.com Unified Payments, Chronopay, CoastalNet, CollectPay (ORCC), CollectPay CC (ORCC), CollectPay Plus (ORCC), Concord/Buypass, CreditGuard, Credomatic Web Service, Credomatic Web Service Dev, CredoRax, Credorax ePower EU – EMV, CredoRax v2, Debiteck, Debiteck 2, Echo CC, ECHO Check, Edelweiss, EFTBOP, LLC, Elavon – EMV, Elavon EISOP UK/EU – EMV, Elavon viaConex, Electronic Check, Electronic Check Multi-Location, eMerchantPay, eMerchantPay Genesis, EPX, Euro Payment, Evertec, EVO, FACe – ProPay, FACe – ProPay ACH, FACe – Vantiv (Next Day Funding), FACe – Vantiv ACH, FACe – Worldpay Core, First Data APACS UK/EU – EMV, First Data Canada, First Data Caribbean V2, First Data Compass, First Data Nashville, First Data Nashville North, First Data Nashville North V2, First Data Omaha, First Data Rapid Connect Cardnet North – EMV, First Data Rapid Connect Nashville – EMV, First Data Rapid Connect Nashville North – EMV, First Data Rapid Connect Omaha – EMV, First Data TeleCheck, First Data TeleCheck Dev, First Data TeleCheck QA, First National Bank of Omaha ACH, Focal Payments, Giact, Global Payments APACS UK/EU – EMV, Global Payments Canada, Global Payments East – EMV, GlobalCollect, Heartland Payment Systems, Heartland Payments Portico – EMV, HSBC Mexico, Ibaro.com, iCanPay, iConsultPay, ICS Access, iNetTrans, Intabill, IntegraPay – Australia/New Zealand, IntegraPay ACH, Interlink, Interlink Intl, IP Pay, iStream ACH, JetPay, KBank, Litle & Co. ACH, Lloyds Cardnet APACS UK/EU – EMV, Maverick Payments LTD, Max Payments, Max Payments Direct, Merchant Partners, Merchant Services Caribbean, MeS Payment Gateway, MeS Trident, Moneris Canada, Moneris US, MPE, MSC Echeck, NCR Payment Solutions, NMI Payments, NPC Electronic Check, Nuvei, Nuvei Digital Payments, OPS-Billing, Optimal Payments, Optimal Payments Canada Check, Optimal Payments Check, PACNET, Pago, PASPX, Paya (formerly GETI), Payliance, Payment Services USA, Payment World, Paymentech Salem Check, Paynamics, Payovation, PayPoint, Paysafe, Paysafe Continuity, Paysafe Continuity Dev, Paysafe Processing PxP, Paysafe Processing PxP Dev, PhoeniXGate, Plug n Pay, PowerCARD, PriceClear, Priority MX Merchant, ProfitStars ACH, Profituity ACH, ProPay, ProPay ACH, PROSA, RS2 Software, RX-Payments, Santander, Secure E-Bill, Secure Payment Systems ACH, SecureNet, Skrill, Speedchex, SRSI-AD, STI, System Merchants, Transact Europe, Transact Pro, TSYS – EMV, TSYS Dev, Turnkey Payments (TPE), Turnkey Payments (TPE) ACH, USAG ACH, Valitor, Vantiv Core Host Capture – EMV, Vantiv Now Worldpay Core – Terminal Capture, Vantiv Now Worldpay eCommerce – Host Capture (Litle & Co), Vantiv Now Worldpay eCommerce – Terminal Capture (Litle & Co.), VegaaH, Ventanex, Vericheck ACH, Vesta, VoicePay, Voicepay Mobile, Walpay, World Pay, World Pay Host Capture – EMV, Worldpay APACS UK/EU – EMV, Worldpay UK CE

✅ Ready to Get Started?

Let Paygen become your smart payment infrastructure. We’re built for scale, flexibility, and transparency.

Recent Comments